For many Veterans across Clifton and North Jersey, homeownership may feel out of reach in today’s housing market. But according to a recent survey from NewDay USA, nearly half of Veterans (49%) believe buying a home isn’t currently possible for them financially.

The reality is many Veterans may be closer to homeownership than they think — especially when they fully understand their VA home loan benefits.

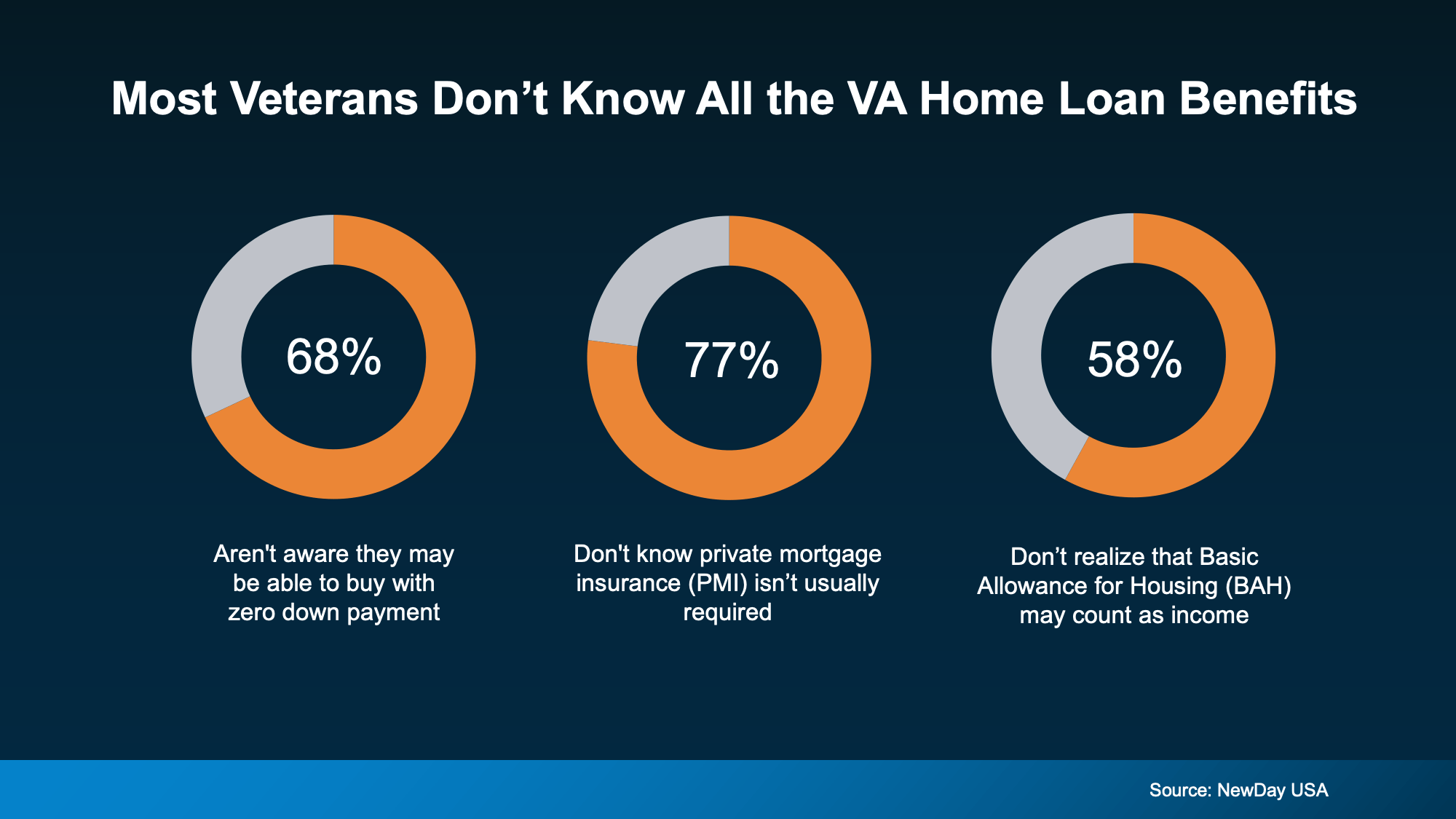

The Veterans Affairs (VA) home loan program has been around for more than 80 years, yet many eligible buyers still misunderstand what these loans actually offer. In fact, three major misconceptions continue to hold Veterans back from purchasing a home.

Many Veterans Don’t Realize a VA Loan May Require No Down Payment

One of the biggest advantages of VA home loan benefits is the possibility of purchasing a home with zero money down. However, many Veterans still assume they need to save tens of thousands of dollars before buying.

According to the NewDay USA survey, many respondents believed they would need between $10,000 and $19,900 saved before purchasing a home. In reality, qualified buyers using a VA loan may not need a down payment at all.

In competitive North Jersey markets like Clifton, Passaic, Nutley, and surrounding communities, eliminating a large upfront down payment can make homeownership much more attainable.

VA Home Loan Benefits May Include Lower Closing Costs

Another advantage many buyers overlook is that VA loans can limit certain closing costs buyers are required to pay.

According to the U.S. Department of Veterans Affairs, there may be restrictions on the types of closing costs Veterans can be charged. That can help buyers keep more money in their pocket on closing day and reduce the amount needed upfront.

Combined with little to no down payment requirements, these VA home loan benefits can help shorten the timeline to homeownership for many military families and Veterans throughout North Jersey.

VA Loans Typically Don’t Require PMI

Unlike many conventional loan programs, VA loans generally do not require private mortgage insurance (PMI), even with low or no money down.

With a conventional loan, PMI can often cost buyers anywhere from $100 to $300 per month until they reach 20% equity, according to NewDay USA. Over time, that can add up to thousands of dollars in additional housing expenses.

For Veterans purchasing a home in North Jersey — where monthly housing costs can already be high — avoiding PMI can make a significant difference in affordability.

BAH and BAS May Help Active-Duty Buyers Qualify for More

For active-duty service members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may also count toward income qualification for a VA loan.

Because BAH and BAS are non-taxable forms of income, they may increase the amount a buyer qualifies for when applying for a mortgage. Many buyers may underestimate their purchasing power simply because they did not factor these benefits into their calculations.

Understanding how these VA home loan benefits work can help military buyers better evaluate their options in today’s North Jersey housing market.

Bottom Line

Many Veterans and active-duty service members may qualify for valuable VA home loan benefits they don’t fully realize are available to them. From potentially no down payment to no PMI and reduced closing costs, VA loans can make homeownership far more achievable.

If you’re considering buying a home in Clifton or anywhere in North Jersey, speaking with a trusted lender and local real estate professional can help you better understand your eligibility and options.

____________________________________________________________________________________________________

About The Source

JK Realty is Clifton’s trusted source for all of your real estate needs and questions. Since 1989 we have been serving the community proudly and look forward to answering any questions you may have…973-472-7000

Contact our agents today or follow up with us on social media for updates and to keep current!